.jpg)

If you’re in the majority of businesses looking to see how investments can create long term value as part of your growth strategy, you really need to know about the new super deduction tax relief.

On 3rd March 2021, the government introduced a temporary super-deduction tax relief to help with business financial recovery from the impact of COVID-19. In addition to this, there is also another temporary first year allowance, the ‘SR allowance’ and a review to the R&D tax reliefs. Businesses really should review if and how they can make the most of these incentives.

What is Super Deduction and Who Qualifies?

Due to the uncertainty and cash restraints on businesses over the last couple of years, business investment has understandably been low on the priority list for a lot of companies. Therefore, to help with the economic recovery from the pandemic the new super deduction capital allowance for capital investments from1st April 2021 until 31st March 2023 will allow companies to cut their tax bill by up to 25p for every £1 they invest.

Companies investing in qualifying new plant and machinery assets will be able to claim:

- a 130% super-deduction capital allowance on qualifying plant and machinery investments

- a 50% first-year allowance for qualifying SR (special rate) assets

The super deduction allowance is only available to companies which are subject to corporation tax and only where the contract for the plant and machinery was entered into after 3rd March 2021 and the expenditure is incurred after 1st April 2021, this also applies to the SR allowance. Companies which do not qualify for the super deduction include individuals, partnerships and LLPs.

Planning to make use of the super deduction or SR allowance? We can help guide you on how to optimise your claims and planned investments. Speak to us today on 01322 555442.

What Investments Qualify for the Super Deduction and SR Allowance?

The Super Deduction applies to new plant and machinery that ordinarily qualifies for the 18% main pool rate for writing down allowances. Examples of qualifying plant and machinery include:

- IT equipment

- Tractors, lorries, vans

- Building equipment, tools and cranes

- Office chairs and desks

- Electric vehicle charge points

- Refrigeration units

- Foundry equipment

- Vehicles used for trading purposes (not cars- they have their own CA rate)

It’s also worth noting that assets that fall into the relevant pools but are used for leasing are excluded from the new allowances.

The SR allowance covers new plant and machinery that qualifies for the 6% special rate pool which includes integral features in buildings such as lifts, heating and ventilation systems and long-life assets.

The best news is that unlike AIA, there is no limit or cap on the amount of capital investment that can qualify for either the super deduction or the SR allowance.

The Super Deduction and Annual Investment Allowance cannot be claimed on the same amount of qualifying expenditure. For all companies that can claim it, the super deduction will be more beneficial than claiming the AIA for a main pool asset purchase. This does not mean that the AIA should be overlooked. In a situation where the contract has been completed prior to 3 March 3 2021, or expenditure predating 1 April 2021 it may still be beneficial to claim the AIA unless the total expenditure on special rate pool assets exceeds the AIA threshold of £1m.

Our Blue Rocket team of expert accountants can help you optimise your claim for super deduction tax allowance. Speak to us today to find out more. Call 01322 555442.

The government has also temporarily extended the period that businesses can carry back trading losses for the relief against profits of earlier years to get a repayment of tax paid. Find out more at gov.uk Temporary extension to carry back of trading losses for Corporation Tax and Income Tax -GOV.UK (www.gov.uk) This measure applies for accounting periods ending in the period 1 April 2020 to 31 March 2022 (and for tax years 2020–2021 and2021—2022 for unincorporated businesses).

How Much Tax Relief Is Given for the Super Deduction?

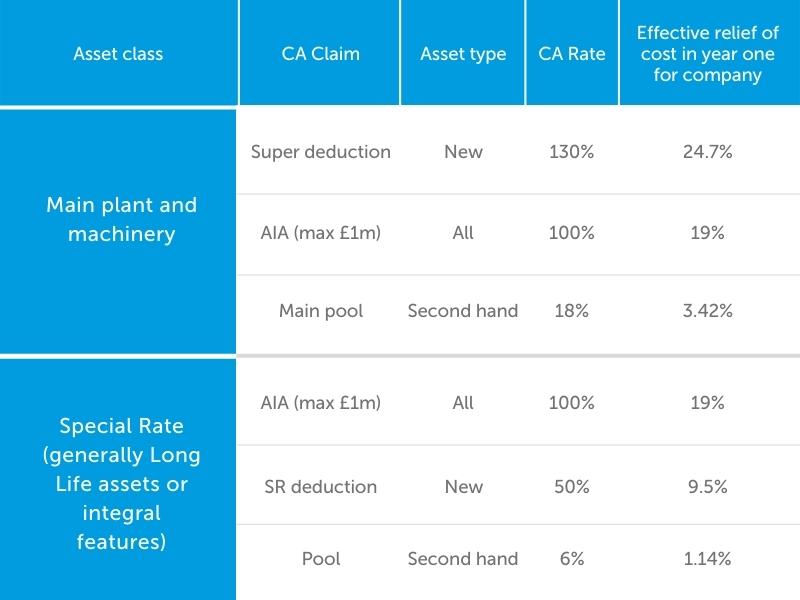

Compared to the usual 18% writing down allowance for the investment in main pool plant and machinery assets, the super deduction gives relief at 130% of the qualifying cost.

The SR allowance gives relief at50% of the qualifying cost in the first year with the balance going into the normal special rate pool to be written down at the usual 6% rate in future years.

Please see the table below for the effective rates of relief for the different claims. With this incentivisation of company expenditure and investment, companies can seize the opportunity to get back to business at full pace. And, with Corporation Tax set to increase to 25% from 2023, careful planning will be needed to ensure that your business benefits from the tax relief allowances available.

If you'd like to understand more about how we can support your business, call us on 01322 555442 or contact us to arrange a free, no obligation initial meeting.